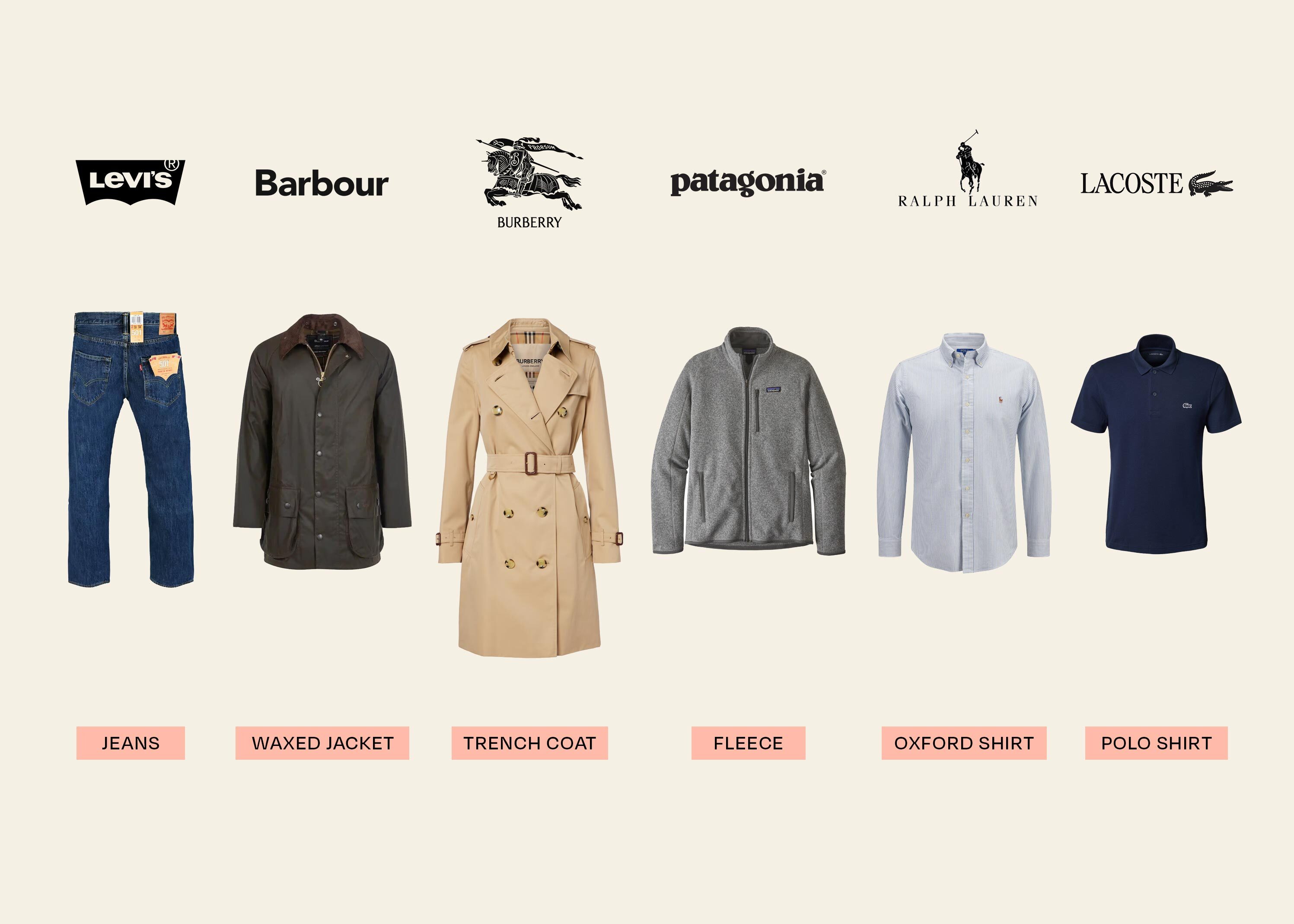

A pattern hiding in plain sight

There are many trench coats, but the category-defining example sits in the public mind under one name. There are many wax jackets, many polo shirts, many oxford button-downs, many loafers, many fleece pullovers, many pairs of five-pocket jeans. In each case the category is generic, the supply is wide and the cost of entry is low. And in each case the typical consumer, asked to picture the category in the abstract, returns the same answer. Trench coat: Burberry. Wax jacket: Barbour. Polo shirt: Lacoste. Oxford shirt: Ralph Lauren. Loafer: Tod's. Jeans: Levi's. Fleece: Patagonia.

The phenomenon does not yet have a precise name in the trade press. "Iconic product" is imprecise, since icons exist in monopolised categories too. "Hero product" is internal retail vocabulary. The most accurate description is the staple item: a product that occupies the mental prototype slot for a generic category, in a market the brand neither invented nor monopolises but quietly defines.

Many makers, one mental prototype

The distinction matters. The Lego brick is not a staple item, because no broad generic category exists alongside it. The Porsche 911 is famous, but the prototypical sports car in the public mind is not consistently the 911. Staple items work differently. They live inside categories with hundreds of credible competitors and dozens of premium ones, and they win the recognition test anyway. The category itself is open. The mental anchor is taken.

The origin-product principle

Most strong staples are also their brand's origin product. Burberry registered its gabardine cloth in 1879 and supplied the British army with the trench coat that gave the category its name. J. Barbour & Sons opened in South Shields in 1894 selling oiled cotton jackets to North Sea sailors. René Lacoste designed the L.12.12 polo in 1933 because tennis whites of the period restricted his serve. Levi Strauss patented riveted denim trousers in 1873, and the 501 lot number followed at the end of the century. Tod's launched the Gommino driving shoe in 1978 with 133 rubber pebbles in its sole. Patagonia introduced the Snap-T and the Synchilla fleece in 1985. The pattern is consistent. The brand and the staple are the same thing seen from two angles.

The economic logic

Jenni Romaniuk's 2018 framework for the Ehrenberg-Bass Institute, Building Distinctive Brand Assets, provides the cleanest reading of the phenomenon. A distinctive brand asset is a sensory cue, paid for over decades, that retrieves the brand from memory at low marginal cost. Logos and colours are the textbook examples. The staple item is the same logic applied at product level. Decades of marketing, retail placement, cultural quotation and editorial coverage have already associated the product with the category. The brand pays nothing further to maintain the association. The staple does the work of recognition by simply existing.

What happens when a brand abandons its staple

The cost of neglecting the staple is visible whenever a brand has tried it. Burberry under Riccardo Tisci and Peter Saville from 2018 onwards is the cleanest case. The new identity moved the trench coat into the supporting cast, retreated from the equestrian knight, demoted the Burberry check and set the wordmark in flat geometric capitals indistinguishable from a dozen luxury peers. The brand spent the late 2010s as a category-anonymous luxury label. The reversal arrives in February 2023 under Daniel Lee. The equestrian knight is reinstated, the serif wordmark recovers, the check returns across product and packaging, and the trench coat is restored to the centre of seasonal communication. The announcement reads in 2023 as a creative-director correction. Read three years later, it is a balance-sheet correction. The brand had subtracted equity from its staple. The deblandification programme is the cost of putting it back.

The staple as commercial backbone

The brands that have actively curated their staples have, by contrast, absorbed cyclical creative shifts without giving up category ownership. Lacoste's April 2026 visual refresh, designed by Commission Studio, treats the L.12.12 as the central exhibit and rebuilds the typography, the crocodile and the green palette around it. Patagonia has continued to put the Snap-T and the Retro-X fleece on its catalogue covers across four decades. Levi's marketing programmes from 2018 onwards re-centre the 501 against the rise of premium-denim challengers. Cross-industry confirmations sit in unrelated categories. The teddy bear is Steiff. The notebook is Moleskine. The ketchup is Heinz. The category in each case is generic and globally contested. The mental prototype is not.

The strategic conclusion

The discipline implied by the staple-item pattern is uncomfortable for many brand owners. It requires admitting that the most valuable single piece of brand equity is often the oldest piece. It requires resisting the periodic temptation to make the staple secondary in service of a fashion narrative or a positioning shift. And it requires the patience to refine rather than redesign, since redesign at staple level forfeits decades of accumulated recognition. The brands that have understood this in the last five years are the ones publishing the most credible identity work today. The brands that have not are the ones now paying to rebuild a category position that they already had, for free, at the start of the decade.

About the author

Brands mentioned in Article

British heritage apparel brand built on waxed cotton craftsmanship, balancing country lifestyle authenticity with contemporary cultural relevance.

5 ArticlesThe originator of the blue jeans, building cultural authority through music, film, and the enduring symbol of the red tab since 1873.

15 ArticlesFounded by tennis champion René Lacoste in 1933, the Maison fuses sportswear heritage with French elegance and is known worldwide for the embroidered …

15 ArticlesFounded by Thomas Burberry in 1856, the British Maison is known worldwide for the gabardine trench coat, the Burberry Check tartan and a heritage root…

18 ArticlesFounded by Ralph Lauren in 1967 with a line of men's neckties, the American Maison evolved from the Polo brand into a global lifestyle business known …

12 ArticlesThe outdoor apparel brand that treats environmental activism as its core business purpose, pioneering sustainability-first brand communication.

7 Articles